Research article link: https://cdhowe.org/publication/big-bang-tax-reform-unleashing-growth-in-the-canadian-economy/ [Below is the introduction and the press release, the 40 page research article is accessible in the attached link.]

- Canada’s tax system has contributed to weak economic performance over the past decade, as the country has recorded the slowest per-capita income growth in the G7 while relying heavily on personal and corporate income taxes that impose relatively high economic costs.

- This report proposes a sweeping, “big bang” reform that would restructure Canada’s tax system to improve growth, reduce distortions, and simplify compliance and administration. At the federal level, it would lower marginal personal income tax rates, introduce an optional simplified $10,000 tax credit to reduce complexity, and overhaul corporate taxation through either a 10 percent “Irish-style” rate with base broadening or a 13 percent distributed profits tax that defers federal taxation on retained earnings until profits are distributed.

- The reform is designed to be revenue-neutral in the short term. To offset lower income tax rates, it would shift toward less distortionary sources of revenue, including either a modest increase in the GST or the introduction of a new employer-paid payroll tax dedicated to healthcare, thereby reducing reliance on economically harmful income taxation.

- Over the long run, the reforms could increase non-residential capital by roughly $140 billion and raise GDP by approximately $79 billion (about 2.5 percent), generating more than $26 billion annually in additional tax revenues while preserving Canada’s strong redistributive outcomes.

Introduction

“For a nation to try to tax itself into prosperity is like a man standing in a bucket and trying to lift himself up by the handle.” – Winston Churchill

Tax policy is a powerful policy tool for shaping an economy. The primary aim of taxation is to raise revenue to fund well-managed public services. However, taxes discourage whatever we choose to tax. Some taxes create more economic harm than others. If governments rely on a poorly designed tax structure to raise revenue, they unnecessarily undermine economic prosperity and make it harder for the economy to sustain the public services voters expect.

After a decade of virtually stagnant per capita economic output, tax reform and broader growth reforms are now on the front burner once again. The need for bold growth-oriented policy changes has become even more acute in light of US “America First” tariff policies, geopolitical tensions, and higher private and public debt financing costs. The federal government promised an “expert review” of the corporate tax system in the last election, but it is absent from its first budget. The budget includes enhanced tax depreciation allowances for a few sectors. We argue that Canada needs a much broader and more comprehensive reform effort.

Several tax reform efforts have been successful in the past. Some were initially unpopular – such as the adoption of the Goods and Services Tax (GST) in 1991 – but were later judged successful because they ultimately improved the economy while providing the government with more stable revenue. The federal and provincial income tax reforms of 1972, 1985–87,[1](javascript:void(0)) and 2000 lowered tax rates and broadened the base, creating a more neutral and fair system that benefited the economy. By contrast, reforms that raise rates or provide preferences for politically favoured activities increase complexity, raise economic costs, and worsen fairness. As American actor and humorous social commentator Will Rogers, once said: “The difference between death and taxes is death doesn’t get worse every time Congress meets.”

In this paper, we propose several “big bang” tax reforms to promote greater Canadian prosperity. We emphasize “big bang” because Canada urgently needs to reorient its economy onto a more prosperous path. These reforms are politically difficult, especially if the aim is to maintain the same level of revenues. The winners from revenue-neutral reform are often silent while the losers strongly oppose any shift in tax burdens. If tax reform is undertaken with some loss in revenue, paired with spending reductions, the reform becomes easier since most taxpayers will be winners.

While our focus is on growth and simplification, we do not ignore fairness. By fairness, we mean both (i) a level-playing field with an equal treatment of equals and (ii) distributing tax burdens according to ability to pay. Canada already achieves the lowest degree of inequality among G7 countries after accounting for taxes and transfers. However, it has also had the lowest per capita growth rates among all G7 countries in the past three decades. Thus, our emphasis is on pro-growth tax reform, given the heightened concern that Canadians have over the economy, with little change in households’ average tax rates.

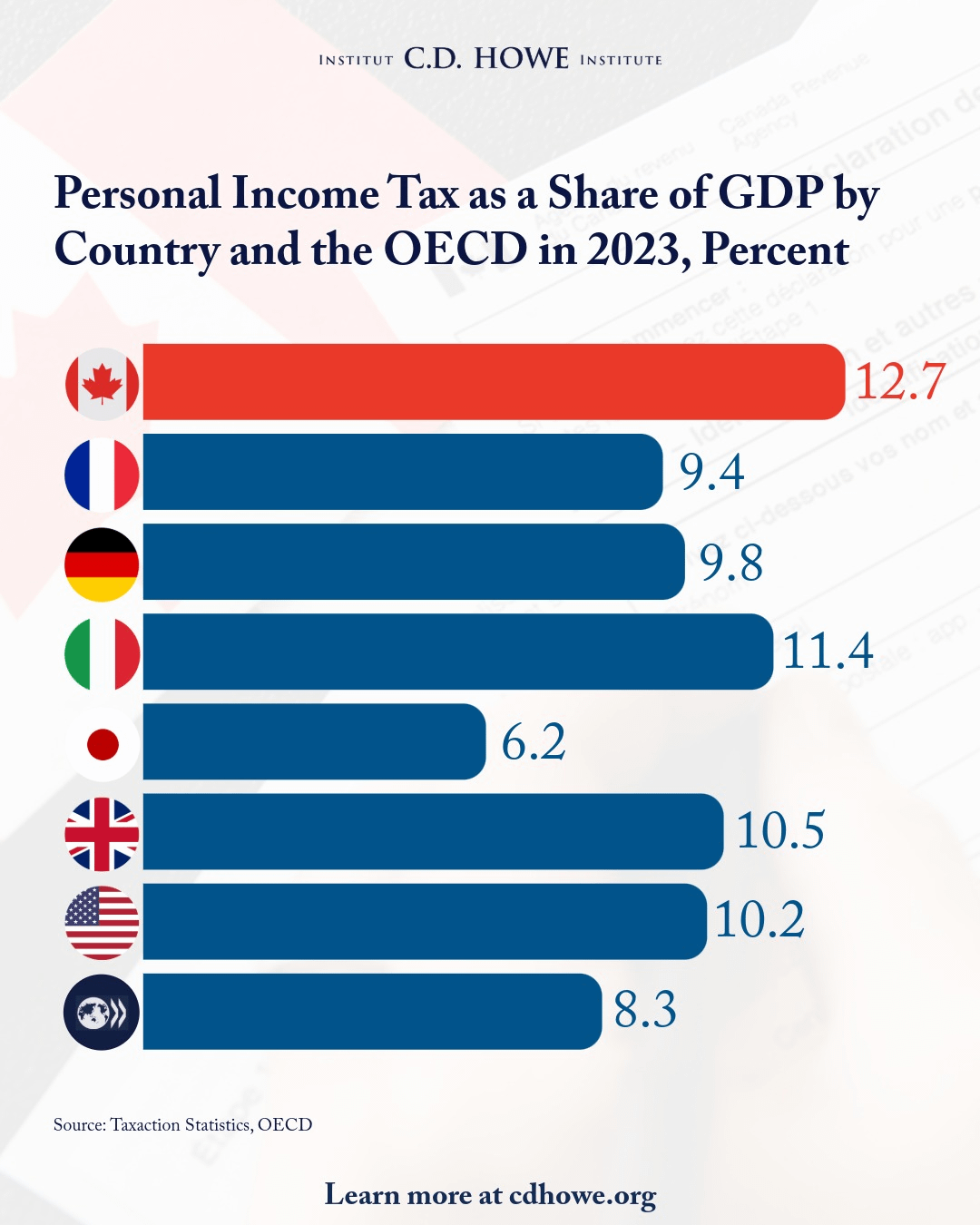

Below, we set out the case for “big bang” tax reform. Canada relies too much on personal income taxes with high marginal tax rates at relatively low levels of income compared to other G7 countries. These rates discourage work effort, risk-taking, and investment, and they encourage Canadians to migrate abroad. The corporate income tax no longer provides an advantage for locating businesses in Canada and distorts the allocation of capital markedly to its most profitable use. Unlike other major countries, Canada relies too little on taxes that cause less economic harm, such as the GST (which itself could be improved) and payroll taxes.

Our “big bang” reform includes four major recommendations that work together as a package while relying less on the most economically damaging taxes, relying more on those that are less harmful, and improving the taxation of corporate income. In designing this package, we have sought to ensure it remains implementable, even if politically challenging, and that does not compromise Canada’s high level of income redistribution:

- Reduce marginal personal income tax rates and widen income brackets. Federal income tax rates would begin at 14 percent for incomes up to $60,000, 20.5 percent for incomes between $60,000 and $180,000, and 26 percent on incomes above $180,000. Provincial rates would apply in addition to the federal rates: the top rate on average would be 45 percent, similar to a decade and a half ago.

- Introduce an optional simplified $10,000 tax credit. Taxpayers could choose this credit instead of itemizing numerous deductions and credits. This policy would especially benefit most low- to mid-income taxpayers and simplify the tax system.

- Reform the corporate income tax to remove preferences. We explore two options. The first reduces the federal corporate income tax rate by five points to 10 percent with the elimination of tax incentives including accelerated depreciation, the small business deduction, and tax credits. The second option exempts retained earnings reinvested in business activities and taxes only distributed book profits at 13 percent. This would result in a substantially lower tax cost on investment for all businesses and encourage venture capital and research. Given that three- to four-fifths of the corporate income tax falls on labour incomes, the reform will improve wages for workers.

- Offset reduced reliance on income taxation by increasing less harmful taxes. We propose either a 2.8-point increase in the GST or a new employer payroll tax at the rate of 3.[2](javascript:void(0)) percent of pay earmarked for healthcare, similar to many European countries and the United States. The payroll tax would apply to payroll and self-employed earnings above $15,000 earned by each individual and therefore fall more on higher earnings.

Our reform will increase investment by $140 billion in the long run and GDP by $79 billion. This analysis holds federal revenues constant in the short term. Naturally, if governments also moderated business grants or other spending, they could reduce taxes further and improve neutrality with respect to business taxation and grant support.

Over time, as economic activity increases due to the tax reform, the reform could yield over $26 billion in additional tax revenues annually across all levels of government.

Press release:

Canada-U.S. free trade is on shaky ground. Canada is not attracting its share of business investment, and our economic performance over the past decade is deeply concerning. We have the weakest growth in per capita national income among G7 countries and several other advanced economies. That’s not a statistical accident but a clear signal the Canadian economy needs a shakeup.

Governments are searching for solutions. But revitalizing risk-taking and entrepreneurship will take more than facilitating “nation-building” projects, eliminating internal trade barriers or layering on new targeted tax incentives. Such measures may help at the margin. But they will not move the dial.

Tax policy is one of the most powerful tools governments have. During last year’s election campaign, Mark Carney’s Liberals promised a corporate income tax review. That is welcome. But Canada needs much more than incremental adjustments to one tax alone. We need a “big-bang” reform that restructures how we tax people and businesses.

Today’s large budget deficits mean reform needs to be revenue-neutral in the short run, even if over time a stronger economy could generate new revenues that ultimately strengthen public finances.

Canada relies more on personal income taxes than any other G7 country. This over-reliance discourages investment, risk-taking and work effort, encourages migration and diverts effort and money toward tax planning rather than productive activity

In a just-released C.D. Howe Institute study, we propose lowering federal personal income tax rates on taxpayers earning above $117,000 — a group that pays roughly 55 per cent of all personal income taxes — and cutting the number of brackets from five to three. The current third, fourth, and fifth bracket rates would fall by three to six percentage points, bringing the combined federal–provincial top rate below 50 per cent in every province.

We also propose a simplified federal tax option that could fit on a single page. Taxpayers could choose a new federal $10,000 simplified tax credit, which would be added to the existing basic personal amount and thus let them earn more than $26,000 tax-free. Only a limited number of deductions and credits would remain: for retirement, charitable donations, disability or caregiving, or expenses incurred to earn income. Other provisions would still be required to avoid double taxation of profits at the corporate and personal levels.

Our estimate is that roughly 90 per cent of taxpayers would choose the simplified tax credit, which would disproportionately benefit lower-income earners, who would pay less tax under it. That nine in 10 filers were choosing the simplified option would reduce and maybe even reverse the political pressure for new boutique credits, opening the way for the system to be simplified once and for all.

We also propose reducing the general corporate income tax rate to 10 per cent for all businesses, large and small, thus eliminating the patchwork of preferences that currently distort business decisions. This lower rate could be financed largely by broadening the tax base: eliminating accelerated depreciation, the small business deduction and various targeted tax credits.

An alternative approach would be a distributed profits tax. It would exempt retained earnings that were reinvested in business activities and tax only distributed book profits. We would suggest a federal rate of 13 per cent.

Either approach would substantially reduce the tax cost of investment, thus encouraging venture capital and innovation. Research suggests most business tax is actually paid by workers, whose wages suffer because taxes depress investment, reducing the demand for workers and leading to layoffs or salary cuts. In a small, open economy like Canada’s, capital can move to wherever it earns the best after-tax return, leaving wages to adjust because labour is less mobile. Lowering the corporate tax burden would therefore support wage growth across the economy. Eliminating corporate tax preferences would also simplify compliance and reduce administrative costs.

To offset lower income tax revenues, Canada should shift toward less distortionary sources of revenue. We propose either a European-style employer payroll contribution for health care or a modest increase in the GST. People may not like consumption and payroll taxes but they do much less economic damage. And the simplified tax credit we propose offsets any harm to lower-income Canadians.

Our proposal’s long-run payoff could be big. We estimate higher investment could raise GDP by roughly $79 billion (2.5 per cent), which would generate more than $26 billion a year in new tax revenues.

We will not reverse Canada’s economic decline with piecemeal tax changes. If we want higher productivity and wages and renewed entrepreneurial dynamism, we need a fundamental re-think of how we tax people and businesses. Canada does not need tax tweaks. It needs a tax re-set.

Posted by IHateTrains123

2 Comments

!ping Can&Tax

Carney is just stealing the conservative playbook at this point.

He just says the right things and doesn’t look like a creep while doing it.