My favorite line from the 1987 movie Wall Street comes when Gordon Gekko ridicules the Charlie Sheen character for his limited ambitions:

I’m not talking about some $400,000-a-year working Wall Street stiff, flying first class, and being comfortable.

Adjusted for inflation, 400K in 1987 would be around $1.1 million now.

What the line tells us that even in 1987, fairly early in the great post-1980 surge in inequality, many people in finance — working Wall Street stiffs — were already being paid very large sums, and a few people were acquiring extraordinary fortunes.

Last week I noted that the very biggest fortunes in America are now primarily based on technology quasi-monopolies. But go down the Forbes 400 list a bit and you see a number of plutocrats who made tens of billions in finance, especially hedge funds. These include people like Stephen Schwarzman, who compared efforts to close a Wall Street-friendly tax loophole to Hitler’s invasion of Poland, and Ken Griffin, a Republican megadonor.

The fact is that financialization of the U.S. economy has been a major driver of rising inequality. What do I mean by financialization? Actually I mean two different but related things. One aspect is the extraordinary rise in the share of the U.S. economy devoted to financial activities as opposed to production of goods and services. A second is the pervasive way in which financiers and financial institutions like hedge funds and private equity have changed how even nonfinancial business operates. These changes have almost always increased inequality.

Beyond the paywall I will discuss the following:

1. The growth of the financial sector and what explains it

2. How growth in finance directly increases income and wealth inequality

3. How the increased role of Wall Street has changed the way the rest of the economy operates

The growth of the financial industry

Banking used to be a relatively boring, sleepy industry. People would talk about “bankers’ hours” — strictly speaking a reference to the days when bank branches were open only from 10 to 3, but informally an implication that banking offered cushy jobs with short hours and not much exertion.

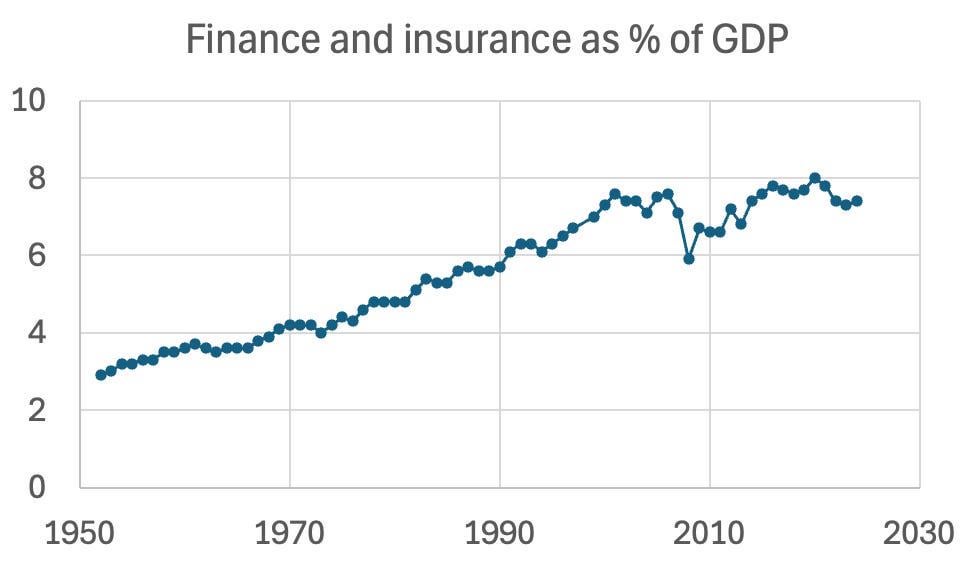

Clearly, that’s not how banking is perceived these days. Investment bankers, especially ambitious young men and women, famously work punishing hours. Today, finance is anything but sleepy. During the 1950s it was a minor part of the economy. By the eve of the global financial crisis, finance’s share of GDP had almost tripled from its 1950s level, and it has remained very high:

Source: Bureau of Economic Analysis

The extraordinary growth of the share of US GDP accounted for by the financial industry raises two related questions. First, what are all these overworked but highly paid people doing? Second, is what they’re doing productive for the economy as a whole?

Bankers, of course, don’t directly produce stuff. However, financial institutions like banks, mutual funds and so on can and do play a crucial productive role in the economy. Ideally, they help direct money to its most productive uses — e.g. effectively channeling household savings into the financing of investment in cutting-edge technologies. Financial institutions also manage risk in the economy by helping investors diversify. And they provide liquidity, giving people ready access to their money even as most of that money is being put to work in long-term investments.

The curious thing is that the financial industry of the 1950s and 1960s, which accounted for 3-4 percent of GDP, served all these functions for the U.S. economy. So why has it expanded to almost 8 percent of GDP? And did this expansion enhance its benefits to the economy?

The outsized growth of the U.S. financial industry can be attributed largely to a change in government policy and, more broadly, the ideological climate that shaped policy. In the 1970s and 1980s, bank regulation was loosened. The Monetary Control Act of 1980 effectively removed limits on the ability of banks to compete with each other by offering higher interest rates on deposits. Even more important, regulators stood aside while the “shadow banking sector” grew. “Shadow banks” are financial institutions like money market funds and overnight lending arrangements that fulfil some traditional banking roles but are neither regulated like conventional banks nor backstopped by deposit insurance. By allowing these shadow banks to displace conventional banking without any major effort to police the new risks these institutions created, policymakers set the stage for eventual catastrophe.

Simultaneously, there was widespread financial “innovation,” largely involving creation of new financial instruments like junk bonds (which had long existed but suddenly became a major force), asset-backed securities, credit default swaps and subprime loans. Again, there was little effort to manage the risks this innovation created.

The proliferation of new financial institutions and instruments, together with the increased role of finance in directing and managing non-financial institutions (more about that later) was a major source of the growth of finance relative to the rest of the economy.

But the important question is whether the huge growth in the financial sector and the financial products it offered was good for the economy. Paul Volcker, the legendary Federal Reserve chairman, famously quipped that

The most important financial innovation that I have seen the past 20 years is the automatic teller machine.

My guess is that today he would include payment apps like Venmo, Apple Pay and Zelle. Yet Volcker’s main point was correct: the U.S. economy did a better job of delivering rising living standards when the financial sector was relatively small and boring than it did after all that innovation came along (I use the log of real income so that the slope of the line shows the rate of growth):

Of course, many factors affect economic growth, so the failure of a larger financial sector to deliver faster growth isn’t proof that it was useless. However, the 2008 financial crisis provided a more pointed rebuttal to claims that financial innovation was an economic boon. Far from helping direct savings to highly productive investments, the deregulated financial system funneled large sums into inflating a disastrous housing bubble. Far from helping to manage risk, financial innovation encouraged both borrowers and investors to take on risks they didn’t understand. And it certainly increased income inequality as subprime mortgages were disproportionately marketed to low and middle income home buyers.

1 Comment

My favorite line from the 1987 movie Wall Street comes when Gordon Gekko ridicules the Charlie Sheen character for his limited ambitions:

I’m not talking about some $400,000-a-year working Wall Street stiff, flying first class, and being comfortable.

Adjusted for inflation, 400K in 1987 would be around $1.1 million now.

What the line tells us that even in 1987, fairly early in the great post-1980 surge in inequality, many people in finance — working Wall Street stiffs — were already being paid very large sums, and a few people were acquiring extraordinary fortunes.

Last week I noted that the very biggest fortunes in America are now primarily based on technology quasi-monopolies. But go down the Forbes 400 list a bit and you see a number of plutocrats who made tens of billions in finance, especially hedge funds. These include people like Stephen Schwarzman, who compared efforts to close a Wall Street-friendly tax loophole to Hitler’s invasion of Poland, and Ken Griffin, a Republican megadonor.

The fact is that financialization of the U.S. economy has been a major driver of rising inequality. What do I mean by financialization? Actually I mean two different but related things. One aspect is the extraordinary rise in the share of the U.S. economy devoted to financial activities as opposed to production of goods and services. A second is the pervasive way in which financiers and financial institutions like hedge funds and private equity have changed how even nonfinancial business operates. These changes have almost always increased inequality.

Beyond the paywall I will discuss the following:

1. The growth of the financial sector and what explains it

2. How growth in finance directly increases income and wealth inequality

3. How the increased role of Wall Street has changed the way the rest of the economy operates

The growth of the financial industry

Banking used to be a relatively boring, sleepy industry. People would talk about “bankers’ hours” — strictly speaking a reference to the days when bank branches were open only from 10 to 3, but informally an implication that banking offered cushy jobs with short hours and not much exertion.

Clearly, that’s not how banking is perceived these days. Investment bankers, especially ambitious young men and women, famously work punishing hours. Today, finance is anything but sleepy. During the 1950s it was a minor part of the economy. By the eve of the global financial crisis, finance’s share of GDP had almost tripled from its 1950s level, and it has remained very high:

Source: Bureau of Economic Analysis

The extraordinary growth of the share of US GDP accounted for by the financial industry raises two related questions. First, what are all these overworked but highly paid people doing? Second, is what they’re doing productive for the economy as a whole?

Bankers, of course, don’t directly produce stuff. However, financial institutions like banks, mutual funds and so on can and do play a crucial productive role in the economy. Ideally, they help direct money to its most productive uses — e.g. effectively channeling household savings into the financing of investment in cutting-edge technologies. Financial institutions also manage risk in the economy by helping investors diversify. And they provide liquidity, giving people ready access to their money even as most of that money is being put to work in long-term investments.

The curious thing is that the financial industry of the 1950s and 1960s, which accounted for 3-4 percent of GDP, served all these functions for the U.S. economy. So why has it expanded to almost 8 percent of GDP? And did this expansion enhance its benefits to the economy?

The outsized growth of the U.S. financial industry can be attributed largely to a change in government policy and, more broadly, the ideological climate that shaped policy. In the 1970s and 1980s, bank regulation was loosened. The Monetary Control Act of 1980 effectively removed limits on the ability of banks to compete with each other by offering higher interest rates on deposits. Even more important, regulators stood aside while the “shadow banking sector” grew. “Shadow banks” are financial institutions like money market funds and overnight lending arrangements that fulfil some traditional banking roles but are neither regulated like conventional banks nor backstopped by deposit insurance. By allowing these shadow banks to displace conventional banking without any major effort to police the new risks these institutions created, policymakers set the stage for eventual catastrophe.

Simultaneously, there was widespread financial “innovation,” largely involving creation of new financial instruments like junk bonds (which had long existed but suddenly became a major force), asset-backed securities, credit default swaps and subprime loans. Again, there was little effort to manage the risks this innovation created.

The proliferation of new financial institutions and instruments, together with the increased role of finance in directing and managing non-financial institutions (more about that later) was a major source of the growth of finance relative to the rest of the economy.

But the important question is whether the huge growth in the financial sector and the financial products it offered was good for the economy. Paul Volcker, the legendary Federal Reserve chairman, famously quipped that

The most important financial innovation that I have seen the past 20 years is the automatic teller machine.

My guess is that today he would include payment apps like Venmo, Apple Pay and Zelle. Yet Volcker’s main point was correct: the U.S. economy did a better job of delivering rising living standards when the financial sector was relatively small and boring than it did after all that innovation came along (I use the log of real income so that the slope of the line shows the rate of growth):

Of course, many factors affect economic growth, so the failure of a larger financial sector to deliver faster growth isn’t proof that it was useless. However, the 2008 financial crisis provided a more pointed rebuttal to claims that financial innovation was an economic boon. Far from helping direct savings to highly productive investments, the deregulated financial system funneled large sums into inflating a disastrous housing bubble. Far from helping to manage risk, financial innovation encouraged both borrowers and investors to take on risks they didn’t understand. And it certainly increased income inequality as subprime mortgages were disproportionately marketed to low and middle income home buyers.