https://thehub.ca/2026/05/06/canadas-real-estate-economy-is-costing-us-heres-how/

As the rhetoric around the federal spring economic update shows, the Carney government has made boosting business investment a centrepiece of its economic aspirations. The ambition is warranted. Non-residential business investment declined for the second straight year in 2025, and Canadian workers now receive roughly 55 cents of new capital for every dollar received by their American counterparts. For machinery and equipment—the tools workers actually use—they get only 41 cents on the dollar.

But the conversation about how to fix Canada’s investment deficit has focused almost entirely on how to attract new capital. It has largely overlooked a more basic question: why does so much of the capital we already have flow into housing rather than productivity-enhancing ventures.

Indeed, Canada has become a “real estate economy” with a major productivity problem. We have built on a foundation that prioritizes shuffling the ownership of existing houses over the productive investment required to grow, and the trade-offs are now impossible to ignore.

The shift in how we deploy capital is stark. In 2000, investment in machinery, equipment, and intellectual property—the key drivers of productivity and long-term living standards—stood at 8.3 percent of GDP, while residential structures accounted for just 4.3 percent. By 2024, those positions had reversed. Residential investment rose to 7.6 percent of GDP, while machinery, equipment, and intellectual property investment dropped to 5.7 percent.

Stripping out intellectual property investment reveals an even sharper decline: machinery and equipment alone almost halved from 6.3 percent to 3.3 percent of GDP, as residential structures nearly doubled.

We are now more concentrated in housing than the United States was at about 6.5 percent of GDP in 2006, just before the crash that triggered the global financial crisis. Our lending rules and banking system are materially different from theirs, but the comparison is still telling.

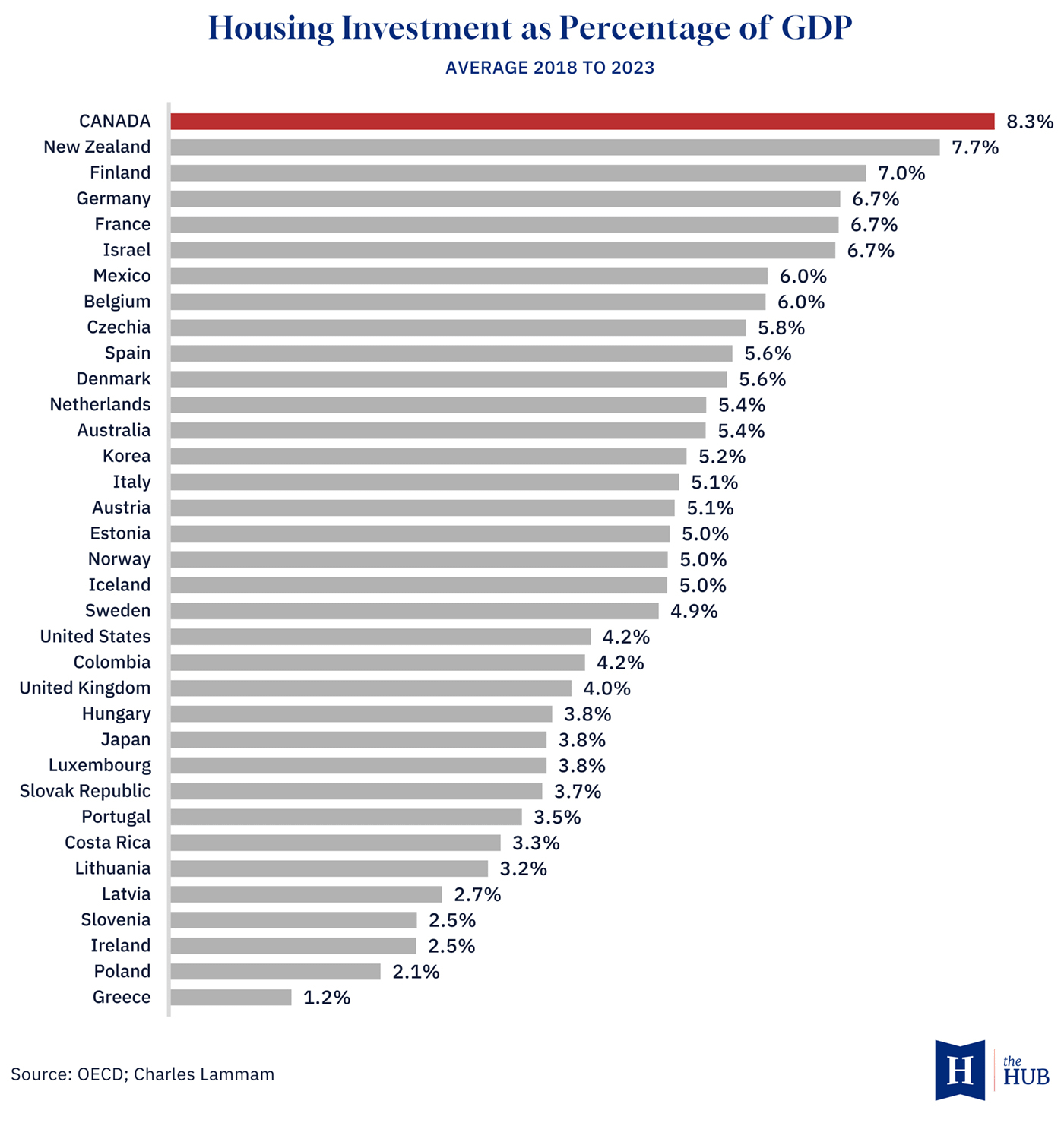

Zoom out and consider how Canada compares to a group of 35 other advanced nations. Between 2018 and 2023, the latest year for which comparable international data is available, Canada dedicated an average of 8.3 percent of GDP to residential investment—the highest of any country—nearly double the U.S. rate of 4.2 percent, and well above Australia (5.4 percent), the Netherlands (5.4 percent), and the United Kingdom (4.0 percent).

But here’s the thing: almost one-fifth of what we record as “residential investment” isn’t really what many of us consider investment. It’s transactional churn. When Statistics Canada calculates residential investment, it includes ownership transfer costs like realtor commissions, legal fees, and land transfer taxes. These services are real, but they create no new productive capital; they simply reflect the cost of moving existing assets from one balance sheet to another. Half of the total residential investment is new construction. Renovations make up about a third.

The consequences show up in our productivity data. Labour productivity in residential construction fell 37.3 percent cumulatively from 2001 to 2023, while the overall business sector saw productivity grow by 12.5 percent. The sector is becoming less efficient at producing output even as it consumes a growing share of Canada’s capital and credit.

The financial system acts as a conduit for the crowding out of business investment. Research from Alberta Central suggests that since the mid-1990s, the household sector has absorbed most of the net lending available in Canada, primarily through mortgages, squeezing the business sector. Government deficits played this role in the 1980s and 1990s; household mortgage debt has played it since.

This partly reflects specific policy choices that tilt the scales. As OSFI Superintendent Peter Routledge has noted, federal banking regulations make mortgage lending significantly more profitable for banks than commercial lending. Due to risk-weight differentials, a bank needs roughly five dollars of capital to back a business loan for every one dollar required for a mortgage. The incentive is compounded by CMHC’s mortgage insurance framework, which backstops lenders against losses while leaving the gains with borrowers and banks.

At the same time, the unlimited principal residence capital gains exemption makes housing the most tax-advantaged asset class in the country. We have structured our financial and tax systems to ensure that capital flows toward bedrooms rather than the machinery and technology that drive long-term prosperity.

The risk is a steady erosion of our economic potential as we redirect income toward debt service and away from productive enterprise. Until we address the structural incentives that have turned Canada into a housing-heavy outlier, we will continue to trade our future growth for a mortgage.

Posted by IHateTrains123

1 Comment

CANADA NUMBER 1!!!! 🇨🇦🇨🇦🇨🇦🇨🇦🇨🇦