Many Canadians are devoting a growing share of their income to paying down debt, and the people now calling in insolvency trustees aren’t who you might expect.

Statistics Canada data show household credit market debt rose to $3.25 trillion in the first quarter of 2026—up 4.4 percent from a year ago. It marked the sixth consecutive quarter in which debt outpaced income growth. The debt-service ratio climbed to 14.75 percent—meaning nearly one in every seven dollars earned is already spoken for before a single grocery is bought or a bill is paid.

The debt-to-disposable-income ratio now sits at 179.6 percent, or $1.80 owed for every dollar of disposable income. Outstanding credit card balances hit a record $124 billion, according to TransUnion’s Credit Industry Insights Report, with 40 to 46 percent of Canadians carrying unpaid balances month to month.

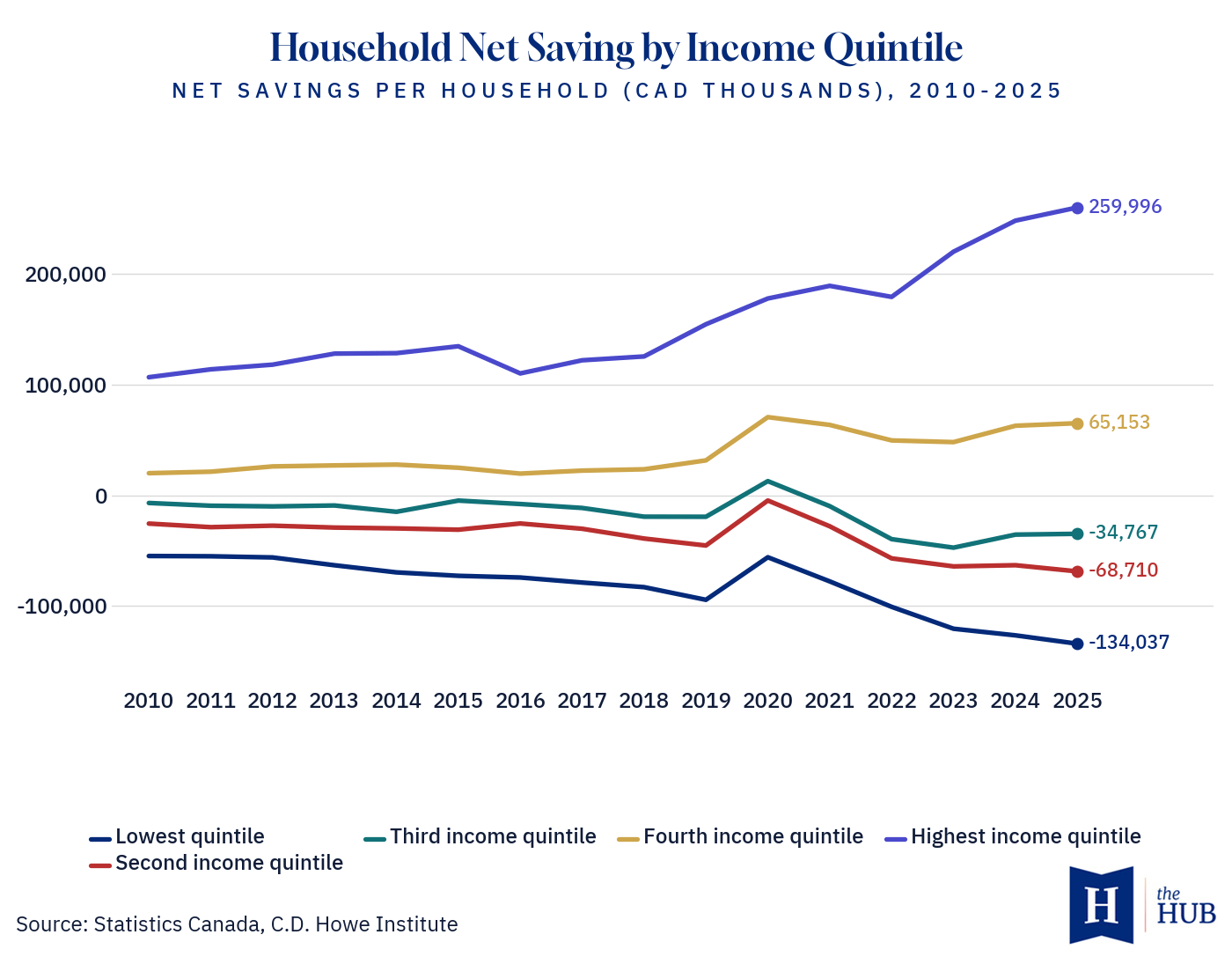

A C.D. Howe Institute analysis published this month found the top income quintile now saves an average of more than $75,000 annually, while the lowest quintile is running a deficit of nearly $39,000 a year—spending well beyond its disposable income. The middle quintiles have also slipped further into the red, a K-shaped divide that the aggregate headline numbers conceal, with all three bottom quintiles in the red.

Homeowners are the new face of insolvency

Scott Terrio, a consumer insolvency counsellor and manager at Hoyes, Michalos Licensed Insolvency Trustees in Toronto, told The Hub the most important story the data is obscuring isn’t the volume of filings—it’s who is filing.

“The big thing we’re seeing now that we weren’t seeing a year ago or a year and a half ago is homeowners calling us,” Terrio said. “That’s the story that the media is completely missing right now. We didn’t speak to homeowners for a decade in this industry because of the housing boom. When houses are going up 20 percent a year, and you’re swimming in equity, you don’t need an insolvency trustee.”

For years, homeowners in financial trouble had a reliable escape valve: refinance, tap a home equity line of credit, and put unsecured debt on the house. That option has largely disappeared as home prices softened, equity shrank, and banks tightened lending. Hoyes Michalos’ Homeowner Bankruptcy Index—tracking the share of the firm’s filers who own homes—has climbed to roughly 11 percent. At its peak in February 2011, it stood at 36 percent.

“We are going to be back at 36 at some point. Guaranteed,” Terrio said.

The index shows insolvent homeowners are carrying an average of nearly $112,000 in unsecured debt on top of their mortgages, and 23 percent of those who filed in 2025 did so already underwater on their home. Young and recent buyers—many of whom got into the market on family-gifted down payments—are disproportionately represented.

“They got in because they got money from family to get the down payment…and now they’re faced with inflation and everything else, and when it comes time to renew the mortgage, and they have to pay $800 more a month or more, they already couldn’t afford the house,” Terrio said.

Homeowners are also a lagging indicator. It typically takes two years for a financially stressed homeowner to file—a combination of psychological resistance, complexity around shared assets, and stubborn hope. The filings visible now reflect distress that began well before the current data.

“It’s not going to be a spike like it usually is,” Terrio said. “It’s going to be a big, long, drawn-out thing because of the homeowners. Instead of a one-and-a-half-year up-and-down spike, it’ll be three, maybe four years.”

The cycle was also distorted by the pandemic. Filings were tracking sharply upward in 2019 when COVID hit, pausing a correction that never arrived. Government assistance left millions temporarily creditor-proof, preventing the usual purge of unsecured debt. That debt remains in the system, layered beneath obligations accumulated through years of elevated food, rent, and energy costs.

Mortgage broker Ron Butler flagged parallel pressure on housing supply. “There are fewer processes in lending that move slower than mortgage default resulting in power of sale action. That’s why it’s unlikely this wave of lenders selling homes has peaked,” Butler recently explained on X.

‘The economy is just not going to go anywhere’

Terrio sees the debt crunch feeding directly into Canada’s economic stagnation.

“A lot of people are using their credit cards to make ends meet. The breaking point will be a combination of maxing out on credit cards and lines of credit—now you can’t do those things. You’re just buying groceries and paying your rent or mortgage, basically. The economy is just not going to go anywhere because nobody’s spending anything more than they have to.”

A third of Canadians are carrying debt on their credit cards month to month.

For households under pressure, Concordia University economics professor Moshe Lander urged a frank accounting of options.

“Households always have options, but that does not mean that they have to like all the options,” Lander said. “Be honest with yourself about what you truly cannot do without and what you merely want to continue doing.”

Lander recommended eliminating recoverable waste—expiring food, unnecessary trips, digital subscriptions—arguing a leaner approach “can bring a surprising amount of savings that may not solve cost-of-living and affordability issues outright, but can certainly provide a cushion and time.”

“If debt is rising as a proportion of income, then the portion of disposable income devoted to debt financing is also rising, which means Canadians must find cuts elsewhere in their discretionary spending,” Lander said. “Unfortunately, there is a limit to how far one can cut. Basic needs like shelter, clothing and food will take increasingly larger portions of that disposable income, and leisure-related spending will be eliminated from the budget.”

Posted by IHateTrains123